Standard Communities, a leading national multifamily housing investor and developer, is developing a ground up 240-unit 100% affordable community in Woodbridge, VA.

The Prince William County project, Jefferson Plaza Apartments, is capitalized at approximately $67.5 million.

Nationally, Standard currently has more than 2,000 units in its new construction pipeline.

Funding for Jefferson Plaza Apartments was secured through Virginia Housing as the issuer of tax-exempt bonds, and Freddie Mac provided Low Income Housing Tax Credits through Hudson Housing Capital.

“Our investment in Woodbridge, VA, is consistent with Standard’s track record throughout the United States of creating high-quality affordable communities,” said Scott Alter, Co-Founder and Principal of Standard Communities. “At Standard, we have a passion for finding innovative solutions to build affordable housing that best serves residents and communities. We are excited to bring new affordable housing to Woodbridge,” said Mr. Alter.

Jefferson Plaza Apartments, at 1305 Jefferson Plaza, will comprise seven 3-story buildings with 147 one-bedroom and 93 two-bedroom units. The community, being built on a 7.6 acre site of a former shopping center, is a transit-oriented development in the Route 1 Corridor within walking distance of the Woodbridge Virginia Railway Express station and close to I-95, with nearby shopping, restaurants and more.

“There is a strong demand for affordable housing in high-cost communities like Woodbridge,” said Feras Qumseya, Standard’s Chief Development Officer. “Developing housing on the site of a former shopping center is not easy, requiring easements and rezoning. The support and assistance from Prince William County to facilitate the process was crucial.” he added.

The property will be income-restricted to 60% of the Area Medium Income, making the units affordable to middle-income families and essential workers.

Jefferson Plaza will feature 354 parking spaces for residents, a 3,000 square foot club room, co-working space, a fitness center, bike storage, a playground and recreational area, greenspace and a dog park. Residents will have direct access to an adjacent park to be built out as part of the project.

“Revitalizing the Route 1 Corridor has been one of my top priorities since being elected as the Woodbridge District Supervisor 4 years ago. The Jefferson Plaza Apartments are a key part of that revitalization effort,” said Jefferson County Supervisor Margaret Angela Franklin. “I would like to thank Standard Communities for investing in Woodbridge. I also would like to thank Christopher Shorter, Prince William County Executive, for the professional staff work that was involved in bringing this much needed project forward,” she added.

“We are proud to provide financing and vital housing tax credits that will help make the construction of 240 new apartment homes a reality,” said Janet Wiglesworth, Interim CEO of Virginia Housing. “Jefferson Plaza will provide an affordable, conveniently located, modern community for residents in Prince William County. It is a product of strong partnerships that have one goal in mind: to invest in the future of affordable housing in our communities.”

Based in New York and Los Angeles, Standard has a national portfolio of almost 20,000 apartment units and has completed more than $4.7 billion of affordable housing acquisitions, rehabilitation and development nationwide. Standard Communities strives to cultivate long-term public and private partnerships to produce and preserve high-quality, affordable and environmentally sustainable housing.

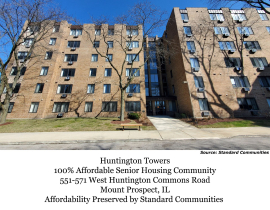

Standard Communities, a major national affordable housing developer and investor, has led a public-private partnership acquiring Huntington Towers, a 100% senior affordable 214-unit community in Mount Prospect, IL. The transaction extends and preserves affordability for 30 years.

The total capitalization of the transaction is approximately $74.9 million, including $16.1 million in planned renovations.

Standard completed the acquisition in partnership with the Illinois Housing Development Authority and the U.S. Department of Housing and Urban Development.

"Our partnership with IHDA and HUD enables Standard to elevate and enhance senior housing in Illinois. By preserving and extending the affordability of this senior community for the next 30 years we ensure a future where our residents thrive in homes that reinforce their independence, community and comfort," said Robert Koerner, Chicago-based Chief Investment Officer of Standard Communities.

Mr. Koerner leads Standard’s Chicago office, which includes his colleagues from Standard’s Acquisitions and Redevelopment, Asset Management, Compliance, Construction and Portfolio Management units.

Located at 551-571 West Huntington Commons Road in Mount Prospect, IL, about 20 miles northwest of Chicago, Huntington Towers was built in 1978.

Standard, with more than 2,400 units in Chicago and its surrounding suburbs, including Bolingbrook, Danville, East Moline, Elgin, Glen Ellyn, Moline and Mount Prospect, has been upgrading and preserving affordable senior and family housing in the area for more than 15 years.

“The acquisition of Huntington Towers continues our growth in the Chicago Metropolitan Area, which is a market we strongly believe in, and plan to invest in long into the future,” said Scott Alter, Co-Founder and Principal at Standard Communities.

“Huntington Towers will continue to offer homes to seniors in an appealing and engaging living environment,” said Thomas Marro, Vice President of Acquisitions and Redevelopment at Standard Communities. “Access to affordable housing is particularly important to seniors living on fixed incomes, and we are eager to transform and elevate this community,” said Mr. Marro.

Renovations at Huntington Towers will include new flooring, kitchen cabinet hardware and solid surface countertops, new ranges, refrigerators and microwaves. Also new toilets, plumbing and grab bars. Light fixtures will be replaced. Hallways will be painted and new carpeting installed. Resident amenities will be enhanced by adding a fitness center and a business center. The exterior will be repaired and a picnic area expanded. A new rooftop solar system will be installed that will produce over 233 MWh of energy annually, reducing the property’s carbon footprint by over 215 tons of CO2 per year. The renovation project will seek Enterprise Green Communities certification which recognizes properties’ holistic approach to green affordable housing.

A Resident Services Coordinator will be added to the staff to assist the residents.

Based in Los Angeles and New York, Standard Communities has a national portfolio of nearly 19,500 apartment units and has completed more than $4.5 billion of affordable housing acquisitions and rehabilitations nationwide. Standard Communities strives to cultivate long-term public-private partnerships to produce and preserve high-quality, affordable and environmentally sustainable housing.

Standard Communities, a leading national developer and investor in affordable and workforce housing, has led a public-private partnership that acquired six 100% affordable Section 8 communities in Los Angeles County with a total of 407 units.

Five of the communities are senior affordable housing.

Standard will extend the communities’ affordability by 20 years under new HUD Housing Assistance Payments contracts.

The transaction has a total capitalization of approximately $122 million, including planned renovation costs of over $8 million. The six communities were built between 1969 and 1980.

“Extending the affordability of all 407 apartment units isn't just a matter of housing; it's a commitment to sustaining the heart of our community. We are not only ensuring that seniors and families have an affordable place to call home, we're also nurturing the vibrant social and economic fabric of Los Angeles County,” said Jeffrey Jaeger, Co-Founder and Principal of Standard Communities. “This investment brings our portfolio in LA County to over 1,700 units.”

The affordable properties in Los Angeles County acquired by Standard include:

· Oxford Park, a 109-unit senior community

· Rayen Park, an 84-unit senior community

· Sherman Arms, a 74-unit senior community

· Villa Marisol, a 48-unit senior community

· Columbus Terrace, a 42-unit senior community

· Villa San Dimas, a 50-unit family community

Standard Communities partnered in this transaction with the non-profit Pacific Southwest Development Corporation.

“Public-private partnerships play a pivotal role in addressing the need for affordable housing. Our partnership with HUD and Pacific Southwest Development on this transaction allows us to preserve hundreds of affordable homes across Los Angeles County,” said Christopher Cruz, Managing Director of Essential Housing of Standard Communities.

Headquartered in Los Angeles and New York, Standard Communities has a national portfolio of over 19,000 apartment units and has completed more than $4 billion of affordable and workforce housing developments, acquisitions and rehabilitation nationwide. One of the 20 largest owners of affordable housing in the country, Standard Communities is a Certified B Corporation. It strives to cultivate long-term public/private partnerships to produce and preserve high-quality, affordable, and environmentally sustainable housing.

Standard Communities, a leading national affordable housing developer and investor, has expanded its principal offices and added staff reflecting robust business.

Standard is one of the 20 largest owners of affordable housing in the United States with nearly 19,000 residential units in its portfolio, an increase of more than 10,000 units since 2021. It has 119 properties across 16 states and Washington, D.C., almost doubling the number of properties under ownership since 2021.

The total capitalization of Standard’s portfolio is approximately $4.4 billion, up from $2 billion in 2021.

“We have applied productive strategies, with acquisitions and ground-up development, to extend our successful track record in a challenging environment,” said Scott Alter, Co-Founder and Principal of Standard Communities. “As a result, we have expanded our three principal offices in New York, Los Angeles, and Washington, D.C., and opened new offices in Miami and Nashville,” said Mr. Alter. Standard’s staff has grown to approximately 90.

In Manhattan and Washington, D.C., Standard recently relocated and expanded its office spaces, more than doubling the size of previous offices in those cities. Its Los Angeles office was extensively renovated.

“Our investment in new and updated office spaces is really an investment in our people and the work they do. In-person collaboration provides significant value and is crucial in fostering effective teamwork and achieving our ambitious goals,” said Mr. Alter.

Standard’s growth includes:

· Breaking ground on two multifamily properties: Aspen Wood in San Ramon, CA and The Line in Savannah, GA

· The largest acquisition in Standard’s history, 28 multifamily affordable properties with 3,151 units in two states.

· Acquisition of Maunakea, the largest FHA deal and biggest Project-Based Section 8 transaction in Hawaii state history.

· Establishing three distinct business lines: Acquisitions & Redevelopment, New Construction, and Essential Housing.

“Public-private partnerships are the most effective way to create, preserve, and improve affordable housing throughout the country. Standard is committed to collaborating with local and state agencies, non-profit organizations and private sector partners, as we help respond to calls for more affordable housing,” said Jeffrey Jaeger, Co-Founder and Principal of Standard Communities.

Headquartered in Los Angeles and New York, Standard Communities has a national portfolio of nearly 19,000 apartment units and has completed more than $4 billion of affordable and workforce housing developments, acquisitions and rehabilitation nationwide. One of the 20 largest owners of affordable housing in the country, Standard Communities is a Certified B Corporation. It strives to cultivate long-term public/private partnerships to produce and preserve high-quality, affordable, and environmentally sustainable housing.

Standard Communities, a major national affordable housing investor and developer, has led a public-private partnership with the State of Hawaii, United States Department of Housing and Urban Development (HUD), Honolulu-based Stanford Carr Development, the City of Honolulu and Hawaii Housing Finance & Development Corporation (HHFDC), in the acquisition of Maunakea, a 379-unit 100% affordable housing community in Honolulu, Hawaii.

This is the largest FHA deal and largest Project-Based Section 8 transaction in Hawaii state history. The transaction extends the affordability of all units at the property for 20 years.

Maunakea, a family community with a primarily senior resident base, is the seventh property in Standard’s Hawaii portfolio which now totals over 1,600 units.

Located at 1245 Maunakea Street in Honolulu, the community has 254 one-bedroom units and 125 two-bedroom units. It was built in 1977 and renovated in 2000. Standard will undertake renovations budgeted at over $41 million, approximately $109,000 per unit.

In unit renovations will include updates to kitchens and bathrooms and new flooring. Residents will also benefit from new windows throughout the property, a new business center, fitness center, and the addition of grills to the picnic area.

“Maunakea is a significant addition to Standard’s robust portfolio of affordable housing in Hawaii, in partnership with an experienced local developer, Stanford Carr. Hawaii has some of the highest rents in the nation, which increases the need for high-quality, affordable housing. We remain committed to uplifting the Honolulu community, and preserving and improving the affordable housing stock is one of the most important ways we can address economic inequalities in the area,” said Jeffrey Jaeger, Co-Founder and Principal of Standard Communities.

Mr. Jaeger pointed out that “this is the first time in decades that state Low Income Housing Tax Credits are available for a 4% tax credit transaction in Hawaii, a state with very limited LIHTC resources. This is a big step toward Standard continuing to preserve affordable housing in Hawaii, positively impacting the lives of residents for years to come.”

“HHFDC is pleased to partner with Standard Communities, Stanford Carr Development and HUD to ensure that all 379 units of Maunakea Tower Apartments are modernized and will remain affordable for many additional years,” said Dean Minakami, HHFDC Interim Executive Director. “Maunakea Tower is a critical component of the affordable housing inventory in Chinatown. Many from our elderly and immigrant populations choose to live in the neighborhood because it is also home to the groceries, herbalists, medical offices and houses of worship that they frequent.”

He added: “This is not the first partnership we’ve had with this team, and we look forward to future endeavors with them.”

In 2020 Standard, also in partnership with HUD, The State of Hawaii and Stanford Carr, closed on an innovative $223.9 million public-private partnership to reposition 1,221 units of affordable housing across six properties located on the islands of Oahu, Hawaii, and Maui.

Headquartered in Los Angeles and New York, Standard Communities has a national portfolio of nearly 19,000 apartment units and has completed more than $4 billion of affordable and workforce housing developments, acquisitions and rehabilitations nationwide. As one of the 20 largest owners of affordable housing in the country, Standard Communities is a Certified B Corporation and strives to cultivate long-term public/private partnerships to produce and preserve high-quality, affordable and environmentally sustainable housing.

STANDARD COMMUNITIES IS THE FIRST NATIONAL AFFORDABLE HOUSING DEVELOPER AWARDED B CORP CERTIFICATION

Standard Communities, a major national affordable housing developer and investor, has been certified as a B Corporation following a rigorous review of the impact of its business model and operations on staff, stakeholders, communities and the environment, consistent with a vision of an inclusive, equitable and regenerative economy benefiting all people, communities and the planet.

B Corp Certification designates that a business meets verified high standards of performance, accountability and transparency. The B Corp verification process is administered by B Lab, a non-profit international network of organizations.

Standard is the first national affordable housing developer to receive B Corp certification.

“High-quality, well-maintained affordable housing is crucial to the well-being and livelihood of so many people. Becoming a Certified B Corporation reflects our commitment to upholding a purpose-driven business and supporting a movement that benefits all through sustainability, transparency and responsible business practices. We will continue to uplift and empower positive change in the affordable housing industry for our residents, our communities and the environment. We are honored to receive this certification and become part of the B Corp community,” said Scott Alter, Co-Founder and Principal at Standard Communities.

Throughout its investments in affordable communities Standard Communities gives the highest priority to environmental sustainability and the safety and comfort of its residents.

Standard Communities has received recognition for its substantial achievements in increasing access to affordable housing across the US and in environmentally responsible investments, leading innovative and successful public private partnerships. These include:

--The Business Achievement Award for Industry Leadership in Affordable Green Housing won by Standard’s affordable housing community Fort Chaplin Park Apartments which has the largest community rooftop solar array in Washington D.C.

--The Novogradac Tax Credit Developments of Distinction Award for Standard's efforts preserving and expanding affordable housing at its Illinois Section 8 Portfolio, an 855-unit portfolio of six properties in the Chicago area.

--The largest tax-exempt bond and LIHTC financed affordable housing transactions in the respective histories of Illinois, California, and Washington, D.C.

--Recognition of Standard as a Great Place to Work, which acknowledges companies that create outstanding experiences for their employees.

“Behind our business, there’s a passionate team helping us achieve our mission of enhancing the quality of life for the residents and communities we serve. We aim to enable every Standard employee to be a force for good and are committed to fostering a supportive and inclusive environment for our team members,” said Joseph Ouellette, Chief Operating Officer at Standard Communities.